And don’t forget that if you’d rather not handle bank reconciliation by hand, accounting software—including free accounting software options—should minimize some of the hassle. This is a simple data entry error that occurs when two digits are accidentally reversed (transposed) when posting a transaction. For example, you wrote a check for $32, but you recorded it as $23 in your accounting software. To do this, businesses need to take into account bank charges, NSF checks, and errors in accounting. Adjust the cash balances in the business account by adding interest or deducting monthly charges and overdraft fees. To learn more about how Clio can help law firms to easily manage trust accounting and three-way reconciliation, while staying compliant, read our guide here.

This includes everything from major fraud and theft to accounting miscalculations, insufficient funds, and incomplete or duplicated payments. Bank charges are service charges and fees deducted for the bank’s processing of the business’s checking account activity. If you’ve irs 1040ez tax form template earned any interest on your bank account balance, it must be added to the cash account. The more frequently you do a bank reconciliation, the easier it is to catch any errors.

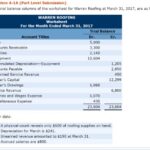

How to perform a three-way trust reconciliation

Resolving the issue could mean paying a bill, depositing a check, or entering a forgotten transaction into your general ledger. The purpose of reconciliation is to ensure the accuracy and ethics of a business’s financial records by comparing internal accounting records with external sources, such as bank records. This process helps detect errors, prevent fraud, ensure regulatory compliance, and provide reliable financial purchase to pay process supply chain overview information for data-driven decision-making. For lawyers, account reconciliation is particularly important when it comes to trust accounts.

- The necessary adjustments should then be made in the cash book, or reported to the bank if necessary, or any timing differences recorded to assist with future reconciliations.

- Since you’ve already adjusted the balances to account for common discrepancies, the numbers should be the same.

- Finally, the reconciliation is reviewed and approved to ensure the financial records are accurate and complete.

- The accountant of company ABC reviews the balance sheet and finds that the bookkeeper entered an extra zero at the end of its accounts payable by accident.

- In general, reconciling bank statements can help you identify any unusual transactions that might be caused by fraud or accounting errors.

In the event that something doesn’t match, you should follow a couple of different steps. First, there are some obvious reasons why there might be discrepancies in your account. If you’ve written a check to a vendor and reduced your account balance in your internal systems accordingly, your bank might show a higher balance until the check hits your account. Similarly, if you were expecting an electronic payment in one month, but it didn’t actually clear until a day before or after the end of the month, this could cause a discrepancy. When you’re performing bank reconciliation, you’re basically following the same process as balancing a checkbook—you’re just doing it on a business-wide scale instead of a personal one.

What is a three-way reconciliation in accounting?

The information on your bank statement is the bank’s record of all transactions impacting the company’s bank account during the past month. Compare the ending balance of your accounting records to your bank statement to see if both cash balances match. Human error in the data entry process can sometimes lead to incorrect amounts or miscalculations on a business’s financial statements. While it cannot entirely erase the potential for data processing errors, using accounting software can reduce the likelihood of errors to help generate more accurate financial statements. And generating financial reports in Clio Accounting is a breeze, making your life, and your accountant’s life that much easier.

During the bank reconciliation process, you’ll compare your bank statements to your business’s financial records. You’ll note any differences between your business’s cash records and your bank’s records, then adjust your internal records to ensure their accuracy. At the end of the process, both your bank account and general ledger (GL) should match, and any differences between the two records should be resolved (or reconciled). Reconciling your bank statements simply means comparing your internal financial records against the records provided to you by your bank.

Non-sufficient funds (NSF) checks are recorded as an adjusted book-balance line item on the bank reconciliation statement. To successfully complete your bank reconciliation, you’ll need your bank statements for the current and previous months as well as your company ledger. An online template can help guide you, but a simple spreadsheet is just as effective. A bank reconciliation statement is a statement prepared by the entity as part of the reconciliation process’ which sets out the entries which have caused the difference between the two balances. It would, for example, list outstanding cheques (ie., issued cheques that have still not been presented at the bank for payment).

Reconciliation in accounting is needed whenever there are financial transactions to ensure accuracy and consistency in the records. It’s typically required at regular intervals, such as monthly, quarterly, or annually, to verify that internal records match external statements like bank accounts, supplier invoices, or customer payments. Reconciliation is also necessary before financial reporting, audits, and tax season preparation. Most importantly, reconciling your bank statements helps you catch fraud before it’s too late. It’s important to keep in mind that consumers have more protections under federal law in terms of their bank accounts than businesses. So it is especially important for businesses to detect any fraudulent or suspicious activity early on—they cannot always count on the bank to cover fraud or errors in their account.

Compare Statements

Whatever method you prefer, it’s important to keep solid records of every transaction to reconcile your bank account properly. If not, you’re most likely looking at an error in your books (or a bank error, which is less likely but possible). If you suspect an error in your books, see posting to the general ledger some common bank reconciliation errors below. Since you’ve already adjusted the balances to account for common discrepancies, the numbers should be the same.

Bank Statement Reconciliation FAQs

There will be very few bank-only transactions to be aware of, and they’re often grouped together at the bottom of your bank statement. Once the balances are equal, businesses need to prepare journal entries to adjust the balance per books. To implement effective reconciliation processes, you need to create and document the exact procedures that staff and lawyers should follow. The accountant of company ABC reviews the balance sheet and finds that the bookkeeper entered an extra zero at the end of its accounts payable by accident. The accountant adjusts the accounts payable to $4.8 million, which is the approximate amount of the estimated accounts payable. However, you typically only have a limited period, such as 30 days from the statement date, to catch and request correction of errors.